National, Regional, and Pennsylvania Context

National Context: Rising Electricity Demand and the Return of Nuclear Energy

The national energy system is entering a period of sustained electricity demand growth. New digital infrastructure is expanding rapidly. Advanced manufacturing is returning to domestic markets. Electrified technologies are increasing power consumption across the United States. Many of these facilities depend on electricity that is reliable and available at all hours. Nuclear energy is re-emerging in this environment as a source of dependable zero-emission power. Today, 94 nuclear reactors at 54 plant sites generate about one-fifth of the country’s electricity, and roughly 45% of the country’s carbon-free power.

Analysis from Grid Strategies found that electricity demand will grow by 166 GW as data centers expand and industrial activity grows [6]. Utilities and policymakers are responding to this shift. Across the country, utilities are planning significant additions of nuclear capacity over the coming decades. Industry projections suggest that as much as 100 GW of additional nuclear generation could be deployed in the United States by the 2050s [4]. Several projects are already advancing. Two commercial reactors are currently under construction, with an additional 30 planned and nearly 500 proposed [5]. Notably, three reactors that previously closed for economic reasons are preparing to restart operations, including Pennsylvania’s Crane Clean Energy Center.

Progress for nuclear energy has been consistent across Federal Administrations. Federal policy is increasingly aligned with this renewed interest in nuclear energy. Congress preserved tax incentives that support both existing nuclear generation and new clean electricity investment. The ADVANCE Act directs the Nuclear Regulatory Commission to modernize licensing processes and improve regulatory efficiency. Federal agencies are also investing in domestic nuclear fuel supply and supporting demonstration projects for advanced reactor technologies. Taken together, rising electricity demand and renewed federal support are creating a new phase of nuclear development in the United States. States that already possess industrial supply chains and nuclear operating experience with trained workforces are positioned to play a central role in that expansion.

Federal Momentum Supporting Nuclear Energy

Federal policy is increasingly aligned with expanded nuclear energy deployment. Policymakers view nuclear energy as an important pathway to strengthen U.S. energy security, maintain global technology leadership, support industrial competitiveness, and provide reliable zero-emission electricity.

Several federal incentives and initiatives now support both the existing nuclear fleet and new nuclear investment.

Federal tax incentives

| 45U Zero-Emission Nuclear Production Credit | Provides up to $15 per MWh for existing nuclear generation through 2032. |

| 45Y Clean Electricity Production Credit | Provides up to $30 per MWh for new clean electricity generation, including nuclear, for projects that begin construction before 2034. |

| 45E Clean Electricity Investment Credit | Provides a 30% investment tax credit for qualifying clean energy projects. Additional incentives may be available for projects located in energy communities or using domestic components. |

Federal financing and investment

Federal financing programs are supporting nuclear deployment and plant restarts, including a $1 billion loan to support the restart of Pennsylvania’s Crane Clean Energy Center.

Congress has appropriated more than $3 billion to expand domestic nuclear fuel supply and strengthen the nuclear industrial base.

Regulatory modernization

The ADVANCE Act directs the Nuclear Regulatory Commission to modernize licensing processes and improve regulatory efficiency for new nuclear technologies.

Federal agencies are advancing reforms related to nuclear energy, national security applications, and supply chain resilience.

Demonstration and early deployment

The federal government has selected 11 pilot projects intended to accelerate new nuclear technologies, with a goal of bringing several projects to operation later this decade.

Private sector and strategic partnerships

Major private-sector partnerships are forming to support advanced reactor deployment in the United States and abroad, including strategic investments tied to Westinghouse reactor technology.

Potential future federal policy

Additional proposals under discussion, such as the Advancing Reliable Capacity (ARC) Act, aim to reduce financial risk for early nuclear deployments and support first-mover projects.

Together, these policies reflect growing federal recognition that nuclear energy will play a significant role in meeting rising electricity demand while supporting U.S. energy security and industrial competitiveness.

Regional Context: A Mid-Atlantic Nuclear Corridor and Pennsylvania’s Right to Lead

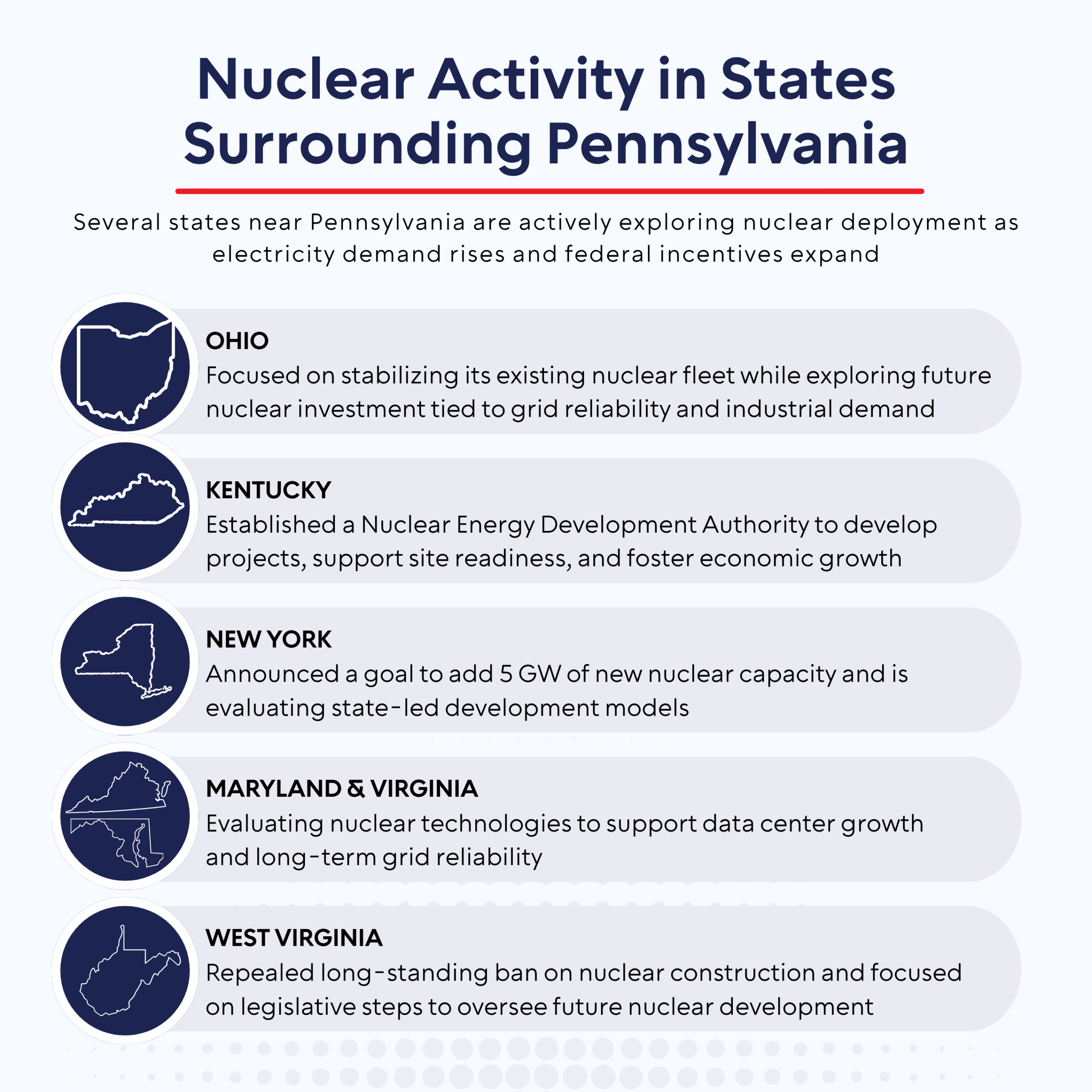

Nuclear energy development is accelerating across the Mid-Atlantic and Midwest. States surrounding Pennsylvania are advancing policies to sustain existing reactors and attract investment in new or additional nuclear capacity tied to rising electricity demand.

Ohio has taken steps to stabilize its nuclear fleet while examining future reactor development. Kentucky recently removed restrictions on nuclear construction and is exploring advanced reactor projects linked to industrial growth. New York has announced plans to pursue new nuclear capacity through state-led initiatives. Maryland and Virginia are evaluating nuclear technologies to support data centers, federal facilities, and long-term grid reliability. These efforts reflect a broader regional shift.

Electricity demand from artificial intelligence infrastructure, advanced manufacturing, and electrification is rising quickly. Nuclear energy is increasingly viewed as one of the few technologies capable of delivering continuous, large-scale power to support that growth. Within this emerging landscape, Pennsylvania occupies a distinctive position. Many states exploring nuclear deployment depend on specialized manufacturing and skilled labor that operate across state lines.

Pennsylvania sits near the center of this regional nuclear ecosystem. Companies and workers in the commonwealth already support nuclear facilities throughout the United States. As new projects move forward across the region, those same capabilities will remain essential. The strategic question for Pennsylvania is therefore not only where reactors will be built, but where the long-term economic value of nuclear development will be captured. Reactor projects create decades of demand for specialized manufacturing and maintenance services.

Pennsylvania has the opportunity to lead the region by strengthening the industrial supply chain and technical expertise that enable nuclear deployment. Reactor projects may emerge in several states. The state that anchors the manufacturing base and talent pipeline will shape the regional nuclear economy. Leveraging Pennsylvania’s existing industrial capacity and nuclear expertise positions the commonwealth to lead that ecosystem while supporting nuclear development across the broader region.

Pennsylvania Context: An Established Nuclear Leader

Pennsylvania has played a central role in the development of nuclear energy in the United States. The nation’s first full-scale commercial nuclear power plant operated in Shippingport, Pennsylvania. Today, the commonwealth hosts eight operating reactors. Another unit is preparing to return to service as the Crane Clean Energy Center. Additionally, nuclear energy supplies roughly one-third of Pennsylvania’s electricity and more than 90% of the state’s carbon-free generation, enough to power 7.3 million homes.[2] Nuclear energy also contributes $2 billion to Pennsylvania’s GDP[1], and has created at least 3,300 direct family-sustaining jobs and nearly 13,000 indirect jobs[2].

Pennsylvania’s leadership extends beyond plant operations. The state maintains one of the deepest nuclear industrial ecosystems in the country. Manufacturers across Pennsylvania produce components, materials, and specialized equipment that support nuclear facilities nationwide. This manufacturing base ranges from large companies that design reactor systems to smaller firms that fabricate valves, forgings, electrical equipment, and other precision components used in nuclear plants. These companies operate alongside plant operators such as Constellation, Talen, and Vistra, forming an integrated nuclear economy that spans generation, manufacturing, engineering, and technical services.

Pennsylvania is also a center of nuclear research and education. Universities across the state support research in nuclear science, materials, and energy systems while training the next generation of engineers and technical specialists. Penn State operates the Breazeale Reactor, the longest continuously operating licensed research reactor in the United States. The reactor serves as a platform for research and collaboration with federal agencies and industry partners. This academic infrastructure reinforces the state’s broader nuclear workforce. Nuclear facilities employ thousands of Pennsylvanians in engineering, operations, and technical roles. Many more workers are employed through supply chains that support plant maintenance, equipment manufacturing, and refueling outages. The concentration of expertise across universities, operating plants, and manufacturers is a defining feature of Pennsylvania’s nuclear leadership.

Pennsylvania’s nuclear history includes the 1979 accident at Three Mile Island Unit 2. The accident produced no detectable health effects among plant workers or the public and led to major improvements in safety culture across the industry.[3] Even so, it remains an important part of the state’s energy history and continues to shape public discussion. Pennsylvania’s location within the PJM regional grid places it within one of the largest electricity markets in the world. The state combines nuclear generation with abundant natural gas resources and extensive transmission infrastructure. These assets position the commonwealth to support rising electricity demand while sustaining a strong industrial base.

For these reasons, Pennsylvania’s nuclear opportunity extends beyond reactor construction alone. The commonwealth’s operating fleet, supply chain capacity, and skilled workforce provide a foundation for long-term participation in the next phase of nuclear energy development.

Why This Moment Matters: A Strategic Window for Nuclear Energy

Electricity demand is rising for the first time in decades while federal policy, private investment, and state strategies are increasingly aligned around nuclear energy. At the same time, several states are moving quickly to position themselves for new projects and supply chain investment. These conditions create a narrow window in which states with existing nuclear industries can translate that foundation into long-term economic leadership.

FOOTNOTES

[1] https://nuclearenergy.pasenategop.com/faqs/

[2] https://www.nei.org/getContentAsset/ec5d3e59-a2bd-498a-bc7c-48d61307ae95/8d8ff8d6-b2ae-401b-a63c-f6b108e809d2/Pennsylvania-State-Fact-Sheet.pdf?language=en-US

[3] https://www.nrc.gov/reading-rm/doc-collections/fact-sheets/3mile-isle

[4] https://www.nei.org/resources/reports-briefs/the-future-of-nuclear-power-2025-survey

[5] https://www.nei.org/advanced-nuclear-energy/advanced-nuclear-project-map

[6] https://gridstrategiesllc.com/wp-content/uploads/Grid-Strategies-National-Load-Growth-Report-2025.pdf

◄ Drivers of the Roadmap | Important Dynamics and Considerations ►