Pennsylvania’s Energy Landscape

What We Know About the Present and Don’t Know About the Future

Seth Blumsack, Co-director, Center for Energy Law and Policy, Pennsylvania State University

Pennsylvania’s regional energy context

Pennsylvania is, and has been for some time, a major energy state. The commonwealth is the second largest overall energy-producing state in the U.S. and the second largest producer of natural gas. Pennsylvania is also routinely among the top three states for electricity production and is one of the largest producers of electricity via nuclear energy. Currently, nuclear and natural gas make up the bulk of electricity generation in Pennsylvania.

Despite the decline in the use of coal for electricity generation, Pennsylvania remains a major coal-producing state. Among states east of the Mississippi River, Pennsylvania ranks fifth in wind energy capacity. Annual wind energy production in Pennsylvania is the second-highest among states on the Eastern Seaboard. Yet even though Pennsylvania is a significant eastern wind-producing state, the role of renewable energy in Pennsylvania’s overall energy mix is low.

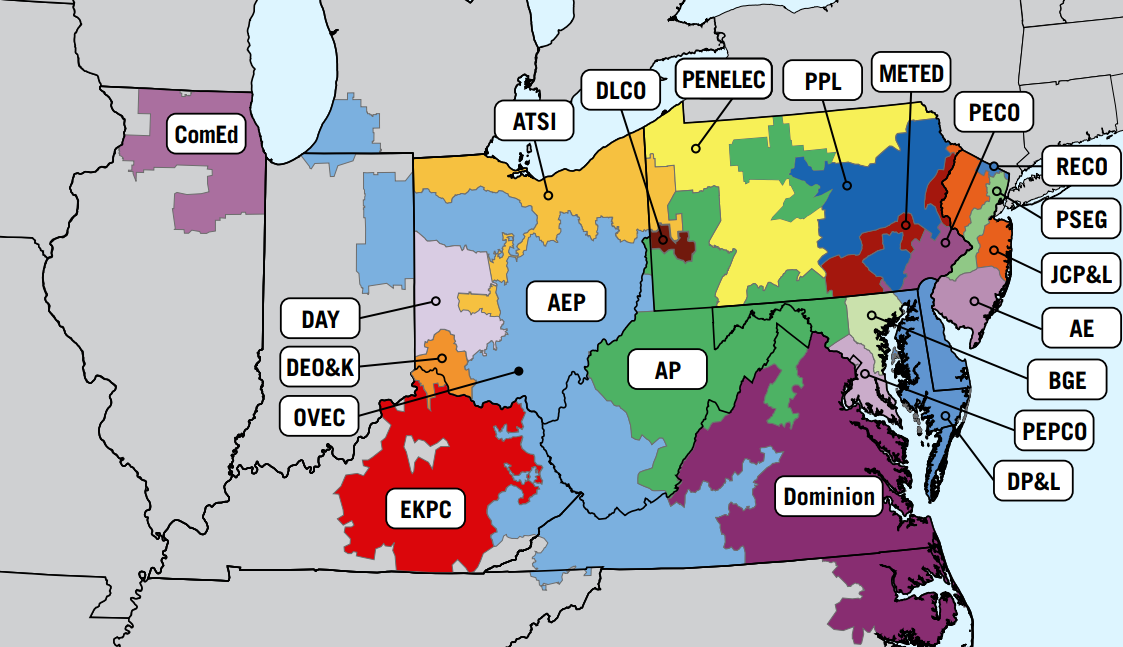

Pennsylvania’s energy sector is not an island – the commonwealth is an integral part of regional energy distribution systems and is a major exporter of energy to surrounding states, particularly natural gas and electricity. Pennsylvania has long been the largest exporter of electricity in the United States and is the second largest exporter of total energy (fuels and electric power together). Pennsylvania’s power generation and transmission infrastructure is part of the multi-state Pennsylvania-Maryland-New Jersey Regional Transmission Organization (RTO), PJM Interconnection LLC (PJM). PJM manages the flow of electricity throughout its footprint, which includes all or parts of thirteen states and the District of Columbia.

While most of Pennsylvania’s electricity exports involve transfers to other states that are part of PJM, it does export some electricity outside of the PJM footprint, particularly to New York. Pennsylvania’s Alternative Energy Portfolio Standard (AEPS), which mandates that utilities purchase or generate a minimum amount of renewable- and low-carbon electricity, was enacted in 2004 and has been updated several times over the past two decades before plateauing in 2021. Governor Shapiro’s administration has proposed a successor policy to the AEPS that would increase the amount of electricity from clean or alternative energy resources by 2035. While the details of these standards vary by state, the majority of states within the PJM footprint have adopted some sort of clean or alternative energy target or goal focused on electricity production.

Pennsylvania’s energy system exists in a context of federal rules and regulations that affect electricity movement, air quality, interstate pipeline siting, the demand for Pennsylvania natural gas for export, and many other things. The Infrastructure Investment and Jobs Act of 2021 and the Inflation Reduction Act of 2022 budgeted billions of dollars to incentivize and accelerate the deployment of clean fuels, low-carbon electricity, and emissions mitigation strategies such as carbon capture, utilization, and storage (CCUS). However, the results of the recent national election have also led to uncertainty about the future of these programs. Sustained national and international demand for US petroleum products and natural gas suggests that traditional energy businesses will continue to underpin key sectors of the global economy for the foreseeable future.

Pennsylvania’s energy future

The future of energy in Pennsylvania will be influenced by a highly diverse set of drivers, including developments in technology, markets and policy. Because of Pennsylvania’s position as a major producer and supplier of energy and electricity to other states, and its participation in regional networks for the distribution of energy and electricity this energy future will also be influenced by policy decisions that are made in other states or at the federal level (in terms of broader energy policy and because PJM is regulated by the Federal Energy Regulatory Commission and not individual states). Changes in the nature of energy and electricity demand that are part of the broader process of energy technology transition are also likely to influence Pennsylvania’s energy sector even if those changes happen most starkly in other states. These factors are also highly uncertain, which complicates the process, but helps underscore the need for developing specific scenarios about the future of energy in Pennsylvania.